Over the last year, house prices have soared. If you’re searching for a new home, it’s not just the purchase price that could be higher. You may also find that Stamp Duty costs are more than you expect.

Having an accurate understanding of the costs of moving home is crucial for effective budgeting. So, here’s what you need to know about Stamp Duty and why the bill could be higher than anticipated.

The average house price has increased by 13% since March 2020

Despite initial concerns that the Covid-19 pandemic would dampen the property market, statistics show the opposite is true.

High demand means the average UK house price has increased by 13%, or £29,000, between March 2020 and May 2022, according to Zoopla research. In the 12 months to May 2022, prices increased by 8.3%.

The competitive market means desirable properties have been selling fast and some buyers have found themselves in bidding wars. As a result, many buyers are finding they need to increase their offers to secure the property they want. It’s a trend that means you may need a larger deposit or mortgage.

However, it’s not just the rise in the purchase price you need to consider. How much the property you’re buying is valued at can affect a whole host of other costs, from solicitor fees to Stamp Duty.

HMRC collected £18.6 billion in Stamp Duty in the year to March 2022

Despite the introduction of a Stamp Duty holiday from July 2020 to June 2021 to support the housing market following lockdowns, HMRC still collected a substantial amount through Stamp Duty.

The Stamp Duty holiday temporarily increased the threshold for paying the tax to £500,000 in England and Northern Ireland. Wales introduced a similar holiday for Land Transaction Tax (LTT), as did Scotland for Land and Building Transaction Tax (LBTT).

In total, in the year to March 2022, HMRC collected £18.6 billion in Stamp Duty, an increase of £6.1 billion when compared to the previous year. And rising house prices suggest Stamp Duty receipts could increase even further in 2022/23.

According to the Zoopla statistics, 4.3 million homes across the UK have been pushed into a higher Stamp Duty tax bracket.

More than a quarter of these properties have now moved above the £125,000 Stamp Duty threshold in England and Northern Ireland. This means around an additional 1.2 million properties would now be liable for Stamp Duty when purchased.

Around 360,000 properties have now been pushed across the tax threshold of £145,000 in Scotland and £180,000 in Wales.

In addition to some properties being liable for Stamp Duty for the first time, around 2.7 million homes are now in a higher tax bracket.

If you’re planning to purchase a new home, understanding how much tax you will need to pay can help you better manage your finances.

When do you need to pay Stamp Duty, and how is it calculated?

Stamp Duty is a tax you pay when purchasing land or property that exceeds a certain threshold.

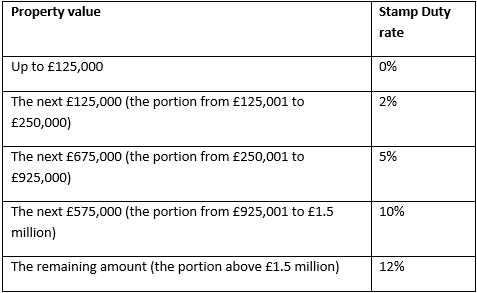

For the 2022/23 tax year, the threshold in England and Northern Ireland is £125,000. The tax rate will depend on the value of the property. Stamp Duty is charged in “slices”. This means you may pay different rates for each part of the property’s value that falls into each bracket.

So, if you purchase a property for £250,000, you will pay no Stamp Duty on the first £125,000, and a rate of 2% on the remaining £125,000. This would result in a Stamp Duty bill of £2,500.

There is a 3% surcharge for additional properties, such as a house you will let out or a holiday home.

If you’re a first-time buyer, you can benefit from a relief that means if you’re buying a property for £300,000 or less, no Stamp Duty will be due. You will also benefit from a lower rate of 5% on the proportion of the property between £300,000 and £500,000.

Your solicitor will usually deal with your Stamp Duty return and make any payment that is due. This must be done within 14 days of the property transaction. Even if the property is under the tax threshold or you will benefit from the first-time buyer relief, you must still submit a return.

If you’re purchasing property in Wales or Scotland, the thresholds and tax rates are different. There are also similar first-time buyer reliefs for LTT and LBTT.

Contact us to discuss your mortgage and property needs

As well as Stamp Duty, there are lots of things to consider when you want to move home. From securing a mortgage to navigating the legal process.

We’re here to help you find a mortgage that suits your needs and offer guidance while you buy your new property. If you’d like to talk to us, please give us a call.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.